How are payday loans calculated?

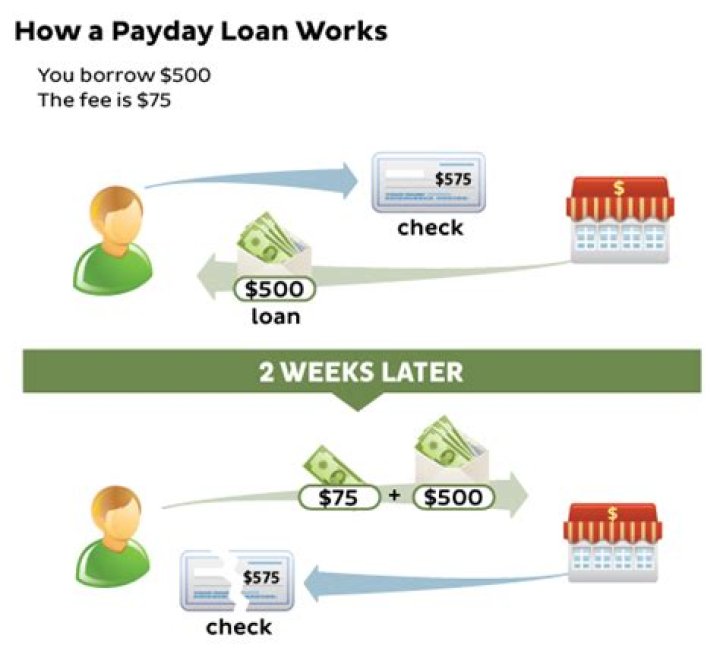

Step 1: Add all fees and interest charges to calculate total fees. Step 2: Divide the total fees by the amount financed (borrowed). Step 3: Multiply the answer by the number of days in a year: 365. Step 4: Divide the answer by the term of the loan in days.

Also asked, how much payday loan can I get?

The amount you can borrow varies by your state's laws and the state of your finances. Most states that allow payday lending cap the amounts somewhere between $300 and $1,000. You can find details on state limits here.

Additionally, how do payday lenders work? A payday loan is an unsecured, high-interest loan with a short repayment period. Borrowers are usually required to make repayments when they receive their salary on their payday, hence the term “payday loan”.

Thereof, what is the average APR on a payday loan?

400 percent

What are the sources of payday loans?

Payday loans are made by payday loan stores, or at stores that sell other financial services, such as check cashing, title loans, rent-to-own and pawn, depending on state licensing requirements. Loans are made via websites and mobile devices. CFPB found 15,766 payday loan stores operating in 2015.

Related Question Answers

Are Payday Loans Worth It?

A payday loan may seem like the only option in a financial emergency if you have poor credit and no savings. But it can do a LOT more harm than good - and there are definitely alternatives. And good for you if you haven't heard of payday loans because they are a really bad idea.Are Payday Loans Easy Pay?

Payday loans are small, short-term fast cash loans. To get a payday loan, you write a personal check to the lender for the amount you are borrowing plus any fees. They can also automatically debit the amount borrowed plus fees if you do not pay back the loan on time and in full.Do payday loans affect your credit?

Payday loans generally are not reported to the three major national credit reporting companies, so they are unlikely to impact your credit scores. Debts in collection could hurt your credit scores. Likewise, some payday lenders bring lawsuits to collect unpaid payday loans.How long do payday loans stay on credit report?

seven yearsAre payday loans harder or easier to pay back?

Payday loans are sometimes harder to pay back than a traditional loan, because the lender did not verify your ability to repay before lending you money. Payday lenders don't generally assess your debt-to-income ratio or take your other debts into account before giving you a loan either.How much can I borrow Check N Go?

In most states, you can get up to $5000 by the next business day with an installment loan. Apply online today using our quick and simple application.Why should payday loans be avoided?

Reasons to Avoid Payday LoansPayday Loans Are Very Expensive – High interest credit cards might charge borrowers an APR of 28 to 36%, but the average payday loan's APR is commonly 398%. Payday Loans Are Financial Quicksand – Many borrowers are unable to repay the loan in the typical two-week repayment period.

Do Payday loans have high interest?

A payday loan is a type of short-term borrowing where a lender will extend high interest credit based on a borrower's income and credit profile. A payday loan's principal is typically a portion of a borrower's next paycheck. These loans charge high-interest rates for short-term immediate credit.What are the legal dangers of payday loans?

These dangers include:- Renewal Fees. When borrowers can't pay back a payday loan on time, they either renew the loan or take out a new one.

- Collections.

- Credit Impacts.

- The Cycle of Debt.

What is a good APR for a loan?

Best personal loan rates in December 2020| Lender | Current APR Range | Loan Term |

|---|---|---|

| Payoff | 5.99%–24.99% | 2 to 5 years |

| Upstart | 7.98%–35.99% | 3 or 5 years |

| LendingClub | 10.68%–35.89% | 3 or 5 years |

| PenFed | 6.49%–17.99% | 1 to 5 years |

Why are payday loan interest rates so high?

Lenders argue the high rates exist because payday loans are risky. Unlike a mortgage or auto loan, there's typically no physical collateral needed. For most payday loans, the balance of the loan, along with the “finance charge” (service fees and interest), is due two weeks later, on your next payday.What does 99.9% APR mean on a loan?

APR stands for annual percentage rate. It's the amount of interest you pay annually on any money you borrow.What is the default rate on payday loans?

The number — 46 percent — is attributed to borrowers who took out multiple payday loans within that two-year period or renewed just one loan. The CRL's study, released Tuesday, goes on to say that of the 46 percent, half defaulted within the first two payday loans they borrowed.What states have banned payday loans?

The states that currently prohibit payday loans are Arizona, Arkansas, Connecticut, Georgia, Maryland, Massachusetts, New Jersey, New York, North Carolina, Pennsylvania, Vermont, West Virginia, and the District of Columbia.What are two advantages of payday loans?

The advantages of taking out payday loans online- You Can Use a Payday Loan for Whatever Purposes.

- Simple Application Process.

- You Can Apply for It Anytime.

- Excellent Option for Emergencies.

- You Can Pick a Repayment Term That Suits Your Needs.

- You Can Track the Outstanding Balance Online.

- The Cost of Payday Loans are Capped by Law.

- Takeaway.

What are two disadvantages of payday loans?

The obvious danger of payday loans is that they can be incredibly expensive to pay off. Borrowers may end up paying more back than they would on other types of loans. Another risk of short-term borrowing is the way it may impact your finances from one month to the next.Can a payday loan sue you?

If you don't repay your loan, the payday lender or a debt collector generally can sue you to collect. If they win, or if you do not dispute the lawsuit or claim, the court will enter an order or judgment against you. The order or judgment will state the amount of money you owe.What apps let you borrow money until payday?

- Earnin. Earnin is an app that allows you to borrow against your next paycheck quickly without any fees or interest payments attached.

- Brigit. Brigit is another app that helps manage your budget and offers cash advances to stretch your funds between paychecks.

- Current.

- Chime.

- MoneyLion.

Do Payday Loans check your bank account?

Here's the reason payday lenders ask for your bank account information. Most payday lenders, whether online or in-store, will likely require your bank account details. This can be frustrating when you're trying to find a quick loan to cover an unexpected expense, but you don't want to share your bank account details.What are the alternatives to payday loans?

Before you take a payday loan, consider one of these eight low-interest payday loan alternatives.- Negotiate a Payment Plan.

- Peer-to-Peer Lending.

- Help from Family.

- Your Own Savings.

- An Advance from Your Employer.

- A Personal Loan or Credit Union Loan.

- A Credit Card.

- Credit Counseling.

How can I borrow $50?

Most lenders don't offer loans as low as $50 — even some payday loan providers.From credit card cash advances to pay advance apps, you have a few different avenues to turn to when looking to borrow $50 fast:

- Pay advance apps.

- Pawn loans.

- Payday loans.

- Credit card cash advance.

- Bank account overdraft.