How do I pay for college Suze Orman?

- UGMA (Uniform Gift to Minors Act Account) or UTMA (Uniform Trust to Minors Act Account):

- Coverdell Educational Savings Account:

- 529 Plans:

Also question is, what does Suze Orman say about 529 plans?

If you make a contribution to a 529 plan, you are not allowed to make a contribution to an education IRA for the same child. For many families, the education IRA is not a very attractive vehicle, anyway. A 529 plan allows you to contribute $100,000 or more for each beneficiary regardless of age or income level.

Additionally, how do I pay for college before tax? If you want to use pre-tax dollars, you can use IRAs, 401(k)s and other qualified retirement plans, which generally allow penalty-free withdrawals for college. However, you won't escape income tax entirely — you will still need to pay income tax on these accounts when you withdraw the money.

In this manner, how do you pay for college plans?

Here are seven other ways to help pay for college:

- Grants. Colleges, states, and the federal government give out grants, which don't need to be repaid.

- Ask the college for more money.

- Work-study jobs.

- Apply for private scholarships.

- Take out loans.

- Claim a $2,500 tax credit.

- Live off campus or enroll in community college.

What is the best way to put money aside for college?

- Open a 529 Plan.

- Put Money Into Eligible Savings Bonds.

- Try a Coverdell Education Savings Account.

- Start a Roth IRA.

- Put Money Into a Custodial Account.

- Invest in Mutual Funds.

- Take Out a Permanent Life Insurance Policy.

- Take Out a Home Equity Loan.

Related Question Answers

How much should I put in a 529 plan per month?

What does this mean for you? Choosing a 529 plan could mean a much lower monthly contribution since the money grows over time. With a 529 plan, solid monthly contribution amounts for a child born in 2017 would be about $165 for a public in-state school, $260 for public out-of-state, or $325 for a private university.What is the point of a 529 plan?

A 529 plan is a tax-advantaged savings plan designed to help pay for education. Originally limited to post-secondary education costs, it was expanded to cover K-12 education in 2017 and apprenticeship programs in 2019. The two major types of 529 plans are savings plans and prepaid tuition plans.Do 529 plans earn interest?

Savings accounts in 529 plans can offer higher interest than at the bank, but fees can affect earnings. A parent who deposits $20 earns interest at the same rate as someone who deposited a total of $100,000.How much should you save per year for college?

Our rule of thumb suggests a savings target of approximately $2,000 multiplied by your child's current age, assuming attendance at a 4-year public college (at $22,180/year), and your family aims to cover approximately 50% of college costs from savings.What you need to know about 529 plans?

A 529 plan allows a participant to set up a tax-advantaged account to allow a beneficiary to use the funds for qualified education expenses. The participant deposits after-tax money in the account. The money in the account can grow tax-deferred and then be tapped tax-free for relevant expenses.What states have 529 plans?

States that offer an income tax benefit for 529 plan contributions- Arizona.

- Arkansas.

- Kansas.

- Minnesota.

- Missouri.

- Montana.

- Pennsylvania.

How do I pay for college if I have no money?

How to pay for college with no money- Identify schools that are or almost tuition-free.

- Apply for federal and state grants.

- Seek out merit-based scholarships.

- Ask for help.

- Trim your academic expenses.

- Consider federal and private loans.

How can I pay for college without my parents help?

- Fill out the FAFSA.

- Apply for scholarships.

- Get a part-time or full-time job.

- Look into tax credits for qualifying college expenses.

- Minimize your college costs.

- Research tuition assistance programs.

- Consider taking out federal student loans.

What is the difference between sticker price and net price for college?

There are two prices for every college degree: the sticker price and the net price. The sticker price is the number that most schools list in their brochures. The net price is that very same number less scholarships, grants and financial aid. It is what you actually pay.How do most students pay for college?

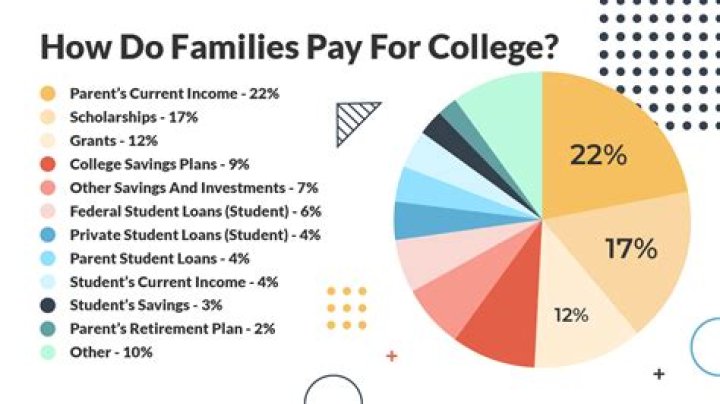

Most students borrow money to pay for college at some point during their education. 20% of parents borrow money to pay for a child's education. 71% of families apply for federal student aid by submitting their FAFSA. 7.7% of loans come from private sources.Is college worth it or not?

It is generally known and accepted that going to university opens the door to better careers, especially in terms of salary. Let's take the United States as an example. Over their careers, Americans with a college degree earn around 570,000 USD more than people who only have a high school diploma.Do you pay college tuition all at once?

Most schools do not require you to pay tuition for the entire year up front. However, if you receive financial aid, the grant or loan you receive typically covers a full academic year.What are 2 benefits of going to college?

10 Benefits of Having a College Degree- Increased Access to Job Opportunities.

- Preparation for a Specialized Career.

- Increased Marketability.

- Increased Earning Potential.

- Economic Stability.

- Networking Opportunities.

- A Pathway to Advancement.

- Personal Growth and Improved Self-Esteem.

How do I pay for college with scholarships?

- Use a free scholarship search site.

- Check out local organizations and nonprofits.

- Contact colleges about institutional scholarships.

- Earn a merit scholarship.

- Apply to scholarships based on majors.

- Take advantage of employer scholarships.

- Try for an athletic scholarship.

Is it better for a parent or grandparent to own a 529 plan?

How Grandparent 529 Plans Affect Financial Aid. Overall, 529 plans have a minimal effect on financial aid. But, the FAFSA treats parent-owned accounts more favorably. For example, you report 529 plans assets as parent assets, which can only reduce aid eligibility by a maximum 5.64% of the account value.Why is a 529 plan a bad idea?

A 529 plan could mean less financial aid.The largest drawback to a 529 plan is that colleges consider it when deciding on financial aid. This means your child could receive less financial aid than you might otherwise need.

Can grandparents get a tax deduction for paying for college?

Can Grandparents Get a Tax Deduction for Paying for College? Grandparents don't qualify for the Lifetime Learning Credit or the refundable American Opportunity Tax Credit unless the grandchild is their dependent. The same rule applies to tuition and fee deductions.Can I use my Roth IRA to pay for child's college?

A Roth IRA is a tax-advantaged retirement account that anyone with an earned income (up to a certain threshold) can contribute to. However, when you withdraw money from a Roth, you can actually use those withdrawals to pay for any expenses, including college expenses for a child or other beneficiary.What happens to money in a 529 plan if not used?

Even if you don't use the funds for your son's education, you still have options. You opened the 529 for the benefit of your son, but the account belongs to you and you have the right to change the beneficiary.Do you get a tax deduction for contributing to a 529 plan?

Although contributions are not deductible, earnings in a 529 plan grow federal tax-free and will not be taxed when the money is taken out to pay for college.Is a 529 account worth it?

Many people saving for college choose 529 plans as their investment vehicles, and that's for good reason. 529 plans offer tax advantages that can help you allocate even more dollars to education expenses. There are a variety of plans available, and you're not limited to just your own state's plan.Is a 529 pre tax or post tax?

While contributions are made on an after-tax basis, the earnings in a 529 plan grow tax-deferred and withdrawals are free of federal income tax when used for qualified higher education expenses.Can you use 529 money to buy a house?

Even if the student were to buy the home, they still can't use 529 plan money to make the mortgage payments. A mortgage payment is a payment on a loan and not a payment of housing costs. If the student owns the home, it may affect the student's eligibility for need-based financial aid.What is the best savings account to open for a child?

Best Savings Accounts for Kids 2021| Best For | Recommended Bank | Opening Minimum |

|---|---|---|

| Best Interest Rate | CIT Savings Builder | $100.00 |

| Best for a Baby | Citizens Bank CollegeSaver | $500.00 |

| Best for Teens | Capital One Kids Savings | $0.00 |

| Best Teaching Tools | PNC S is for Savings | $25.00 |

How much can you put in a 529 per year?

This includes 529 Savings Plan contributions. In 2018, an individual can give an annual gift of up to $15,000 to a person without paying taxes. If the gift exceeds $15,000, then the donor (not the gift recipient) may be required to pay taxes on the gift amount. For a married couple, this amount doubles.What is the best account for college savings?

But 529s and ESAs are generally considered better choices for college savings because of their tax advantages. There are two types of tax-advantaged college savings plans designed to help parents finance education: 529 Plans and Education Savings Accounts (also known as ESAs or Coverdell accounts).What are the disadvantages of 529 plan?

Here are five potential disadvantages of 529 plans that might affect your savings choice.- There are significant upfront costs.

- Your child's need-based aid could be reduced.

- There are penalties for noneducational withdrawals.

- There are also penalties for ill-timed withdrawals.

- You have less say over your investments.

What can you spend 529 money on?

- Qualified expenses that 529s cover. A tax-advantaged 529 college savings plan can be used to pay for college, but not all expenses qualify.

- College tuition and fees.

- Vocational and trade school tuition and fees.

- Elementary or secondary school tuition.

- Off-campus housing.

- Food and meal plans.

- Books and supplies.

- Computers.

What is the best college fund for a child?

A 529 plan is one of the best, tax-advantaged ways to save for higher education costs. Traditional and Roth IRAs can be used to pay for college expenses, but parents should be sure their retirement needs are covered. Coverdell ESAs allow you to set aside $2,000 per beneficiary per year.What are the best performing 529 plans?

Top 10 performing 529 college savings plans| Rank | State | Plan |

|---|---|---|

| 1 | Nevada | USAA 529 College Savings Plan |

| 2 | Maryland | Maryland 529 -- Maryland Senator Edward J. Kasemeyer College Investment Plan |

| 3 | Alaska | Alaska 529 |

| 3 | Alaska | T. Rowe Price College Savings Plan |